ASSESSMENT OF THE CREDITWORTHINESS OF INDIVIDUAL BORROWERS IN BANKING PRACTICE

Конференция: CV Международная научно-практическая конференция «Научный форум: экономика и менеджмент»

Секция: Финансы, денежное обращение и кредит

CV Международная научно-практическая конференция «Научный форум: экономика и менеджмент»

ASSESSMENT OF THE CREDITWORTHINESS OF INDIVIDUAL BORROWERS IN BANKING PRACTICE

ОЦЕНКА КРЕДИТОСПОСОБНОСТИ ЗАЕМЩИКОВ-ФИЗИЧЕСКИХ ЛИЦ В БАНКОВСКОЙ ПРАКТИКЕ

Жарыкбасова Асима Ерлановна

студент, Евразийский национальный университет имени Л.Н.Гумилева, Казахстан, г. Астана

Сапарова Ботагоз Сергазиевна

канд. экон. наук, Ph D, проф., Евразийский национальный университет имени Л.Н.Гумилева, Казахстан, г. Астана

Abstract. This article analyzes the issue of assessment of creditworthiness of individual borrowers in banking operations through the case study of JSC ForteBank. The research evaluates the main indicators that used to assess the creditworthiness of a borrower and determines features of applying these indicators in deciding on giving credit. Thus, it has been proved that the most important indicators for creditworthiness of a borrower include income of a borrower, his indebtedness and credit history.

Аннотация. В статье рассматривается оценка кредитоспособности заёмщиков-физических лиц в банковской практике на примере АО «ForteBank». Проведен анализ показателей, применяемых при оценке заёмщиков и определены особенности их применения для принятия кредитных решений. Установлено, что наибольшее значение имеют доход заёмщика, долговая нагрузка и кредитная история, а применение скоринговых моделей повышает эффективность оценки.

Keywords: creditworthiness of a borrower, credit risk, debt burden, scoring models, assessment of borrowers.

Ключевые слова: кредитоспособность заёмщиков, кредитный риск, долговая нагрузка, скоринговые модели, оценка заёмщиков.

In recent years, the expansion of consumer lending and the growth of the banking sector have proceeded intensively. In this regard, it is especially important to conduct a qualitative evaluation of creditworthiness. The development of consumer lending positively affects the improvement of the living standard of borrowers. Also, it increases the likelihood of credit risk. Thus, it is necessary to pay increased attention to developing new approaches and tools that will enable the bank to estimate the level of creditworthiness of borrowers accurately [2, p.1].

The relevance of the theme is conditioned not only by the development of the financial sector but, also, by changes in regulation. The standards of the Basel Committee on Banking Supervision indicate the necessity of conducting a comprehensive evaluation of borrower’s solvency and improving the accounting for credit risks in banking practice. It becomes more relevant with growing household debt loads and economic instability [4, p.152]. Digital technology, in addition, is changing the approaches to estimating the level of creditworthiness of clients. Currently, banks use additional information about borrower behavior that can be acquired with the use of advanced technologies for analyzing digital data in their decision-making process [1, p.13]. Thus, there is a need to review and improve the approaches to using creditworthiness indicators of individual borrowers, considering modern tendencies in the development of banking system.

It is needed to conduct an analysis of the use of creditworthiness indicators in the practice of banks and to highlight the features of their consumption with the help of the case of JSC ForteBank.

JSC ForteBank is one of the main commercial banks in Kazakhstan, which functions according to the license issued for it. It is notable that this commercial bank provides both physical and juridical entities with its banking products. The bank has a wide net of branches that makes services accessible to people and allows extending retail lending. The bank’s head office is situated in Astana, and the activities of JSC ForteBank are implemented in a centralized way. Decisions about the credit policy, risk limits, and scoring models are made in the head office of the company, while the activities of individual branches including providing banking services and support to clients in loan applying processes.

The bank’s activities have become increasingly interrelated with digital technologies over the last few years. The introduction of digital tools for processing loan applications, automated assessment systems and online services has improved the speed and availability of banking service [3, p.115]. The process of credit decision-making becomes more automated. In this case, it considers information about an individual, including their income, credit history and current obligations. Therefore, the operations of JSC ForteBank are conducted in conditions of growth in retail lending and strengthening of requirements for credit risk management. In this context, the assessment of borrower’s creditworthiness is especially crucial.

The role of the indicators employed in its implementation is growing. Global experience demonstrates that borrowers are assessed on an integrated basis – financial, behavioral and risk-based indicators are analyzed (the analysis of the bank’s activities was conducted by JSC ForteBank). The primary parameters are the level and stability of income of an individual whom the loan is issued, indicators of its debt load (DSR, DSTI), credit history and behavioral factors. Credit risk indicators are also performed, including probability of default (PD), loss given default (LGD) and exposure at default (EAD) which is executed by IFRS 9 (International Financial Reporting Standards).

Table 1 shows the key indicators of borrower’s creditworthiness and their application.

Table 1.

Indicators of borrower’s creditworthiness and their application in JSC ForteBank

|

№ |

Group of indicators |

Content |

Practical application |

|

1 |

Financial |

Income, stability, employment |

Determining the borrower's ability to service the debt |

|

2 |

Debt burden |

DSR/DSTI, current loans |

Limitation of the loan amount |

|

3 |

Credit history |

Delays, discipline |

Assessment of the borrower's credit discipline |

|

4 |

Behavioral |

Activity, stability |

Application of scoring models for automated assessment |

|

5 |

Risk indicators |

PD, LGD, EAD |

Assessment of risks and reserves |

According to table 1, the bank employs a multifactor assessment system which evaluates borrowers through multiple indicators to reach its decision. The primary role of this system depends on both debt burden measurements and credit history records. The additional indicators function as secondary elements which improve the complete evaluation process.

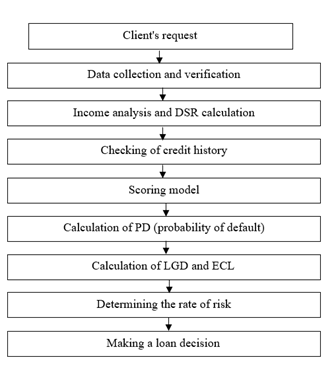

The assessment of borrower’s creditworthiness occurs through numerous stages which lead to consistent decision-making based on reasonable grounds. The figure illustrates the main stages which define this process.

Figure 1. The process of assessing the borrower's creditworthiness in ForteBank JSC

The figure shows that the process used to evaluate borrowers, consists of the multiple assessment stages which involve both financial indicator evaluation and scoring model implementation. The rising demand for retail lending services makes it essential to assess borrower creditworthiness with precise accuracy. The loan portfolio quality depends more on proper client selection when the organization experiences higher loan volume growth especially with consumer loans. Any minor mistake in valuation will result in higher demand which forces the company to increase its reserves while its profit margins decrease. Therefore, risk-based indicators must be implemented as a crucial tool. The assessment evaluates the borrower’s present status and the potential bank losses. The figure 1 shows that the indicators conduct PD, LGD, ECL calculations which influence the credit decision-making process.

The borrower credit evaluation system at JSC ForteBank operates as a complete system which functions is to handle credit risk assessment to produce accurate loan decision results.

The credit evaluation process at JSC ForteBank shows that its success depends mainly on the effectiveness of the indicators used during the evaluation. The loan portfolio expansion together with the high consumer lending volume requires precise assessment methods for evaluating borrowers. The system effectiveness evaluation will use credit risk assessment indicators which is demonstrated in table 2.

Table 2.

Assessment of the quality of the loan portfolio of JSC ForteBank

|

№ |

Indicator |

2022 year |

2023 year |

2024 year |

Economic characteristics |

|

1 |

credit portfolio |

1,1 trillion tenge |

1,37 trillion tenge |

1,82 trillion tenge |

High volume of loans |

|

2 |

Consumer loans |

350 billion tenge |

420 billion tenge |

486 м billion tenge |

A significant proportion of unsecured loans |

|

3 |

NPL ratio |

|

|

~3,6% |

Moderate level of problem debt |

|

4 |

Reserves (ECL) |

|

|

~95 billion tenge |

Formation of reserves for risks |

|

5 |

PD/LGD |

|

|

wide range |

Differentiation of borrowers by risk |

Table 2 shows that problem debt levels stay moderate because lending volumes have increased. The borrower assessment system proves effective since it successfully evaluates its users. The study uncovered special features which determine how credit indicators should be applied. Decision-making depends on three main factors which include the borrower’s income and debt burden and credit history. Scoring models enable to process applications faster and standardize the assessment approach. The system still has various limitations. The assessment depends on the reliability of information about the borrower’s income. The risk level increases when there is a high amount of unpaid loans. The assessment of costumer solvency will decline because economic conditions will cause financial difficulties for costumers.

The analysis demonstrated that bank assess borrower’s creditworthiness through interrelated indicators. JSC ForteBank applies a comprehensive methodology which combines financial rates, behavioral and risk assessments criteria. The system supports multiple methods for assessing the financial capacity of borrowers. The most important factors that influence loan approval decisions include the borrower’s income level and debt obligations and their past credit performance. The scoring models enable to automate their assessment procedures while achieving higher operational efficiency. Certain limitations related to the dependence of data reliability assessment, a high proportion of consumer lending and the influence of external economic factors have also been identified.

The credit assessment system at JSC ForteBank shows operational effectiveness. Nevertheless, it needs ongoing enhancements with the regard of the changes in the economic environment and borrower.